Whitepaper

The Fractional Reserve Stablecoin: The Natural Evolution of Modern Banking Introducing InfiniFi, the first fractional reserve stablecoin to secure greater returns without increased risk by better addressing banking’s duration gap problem.Abstract

For the vast majority of history, the world’s financial capital has rested on a flawed foundation. Today, nearly all modern government treasuries and private financial institutions rely on fractional reserve banking. Banks use past behavior to predict how much of their customers’ deposits to keep on hand while lending out the rest to secure greater returns. This can lead to greater capital efficiency and economic expansion in the regions they serve. However, fractional reserve banking also creates duration gaps — a mismatch between the average maturity of a bank’s liquid liabilities and illiquid assets — which can lead to insolvency if enough depositors attempt to withdraw their money at once. To account for those duration gaps, banks must efficiently manage their balance sheets, effectively model cash outflows, and appropriately handle coordination failures that could lead to bank runs. However, they have imperfect solutions for doing so, relying on reactive lookback models and centralized planning models that misalign incentives between them and their depositors. This leads to increasing threats to the integrity of the global financial system, as witnessed in 2023, the biggest year ever for bank failures, with five banks managing a record $548.7 billion collapsing (led by First Republic Bank, Silicon Valley Bank, and Signature Bank, which represented the second, third, and fourth-largest bank collapses ever). We propose InfiniFi, a fractional-reserve stablecoin powered by a self-coordinated, duration-matching autonomous balance sheet to directly measure market sentiment and address the problems posed by duration gaps. This depositor-directed system decentralizes how assets are allocated, giving individual depositors choices based on their specific risk, duration, and liquidity preferences. This allows InfiniFi to create more proactive models that better forecast depositor behavior and reduce the risk of coordination failures and bank runs. By better addressing the duration gap, InfiniFi more efficiently deploys capital, allowing it to generate higher returns for any existing asset without increased risk. As such, InfiniFi represents a generational opportunity to move our shaky financial system to steadier ground, while also providing the first major incentive to tokenize all assets on blockchain technology.1.0 The fracturing of the fractional reserve system

Fractional reserve banking has existed for centuries. It relies on the fact that depositors do not generally ask for all of their money back at once. That means shrewd bankers can lend out a significant portion of those deposits and generate high returns, so long as they keep enough cash on hand to cover expected withdrawals. Rather than deploying all of their cash deposits into liquid assets that can immediately be redeemed for cash, such as treasury bills, banks that use fractional reserve deploy a portion of deposits (typically the majority) into illiquid assets, such as loans, that cannot immediately redeemed but pay higher returns to compensate for the increased risk they represent. This allows banks to increase their returns above what would otherwise be achievable in fully liquid assets. This increase in capital efficiency comes at a cost. The vast majority of depositor obligations held by banks (their liabilities) are fully liquid (90%) and may be redeemed at any point in time. However, the illiquid assets held by banks have a duration associated with them that must pass before they reach maturity. The mismatch between these zero-duration liabilities and these positive-duration assets is termed the “duration-gap” and serves as the core problem that most banking infrastructure has been built to address. Since banks do not have cash on-hand to cover depositor obligations, they must design and operate systems that manage this shortcoming. Any entity utilizing a fractional-reserve system must determine how to select assets to ensure that daily cash inflows are sufficient to match projected outflows, how to model and predict what those projected outflows will be, and how to respond when outflows far exceed inflows and a bank run begins. For traditional banks, these problems are addressed with hierarchical balance-sheet management, look-back models trained on past data, and a government-sponsored insurance framework. This traditional approach is as good as the tools of the time have allowed but is neither efficient nor sufficient.1.1 The misaligned incentives of centralized balance sheets

To ensure that the existence of the duration gap does not result in the insolvency of the bank, institutions utilizing fractional reserve systems must determine which assets to select such that daily cash inflows from those assets reaching maturity are roughly equivalent to daily cash outflows. This process of selecting illiquid assets to reach maturity at a certain rate over a given period of time is known as “laddering,” and serves as an important and labor intensive task for any bank.This task of balance-sheet management necessitates an organized approach to address it, and to this end, banks use a top-down hierarchy. Upper management breaks the task of laddering into sub-tasks, then hires employees to perform these sub-tasks, rewarding and promoting the employees whose decisions result in better outcomes for the bank. This is an efficient and time-tested approach to solving complex problems such as laddering, but unfortunately, the top-down approach that banks utilize to address laddering results in the creation of perverse incentives. As employees are rewarded for producing the best outcomes for their employers, they are encouraged to pursue goals that will provide the best outcomes for the bank, rather than the depositors. This incentive misalignment encourages bankers to pursue balance-sheet management strategies optimized purely for high returns, which directly make the bank more money, rather than optimizing for a balance of risk and reward. With high return strategies comes higher risk, but if the strategies which bankers are incentivized to pursue result in loss of depositor capital and bank failure, the penalty to any individual banker is negligible, as the Global Financial Crisis highlighted (2008). While many individual bankers doubtlessly find the incentives their system creates concerning, those who might otherwise pursue more conservative strategies are put in a situation where they must choose between pursuing higher risk strategies, or hamstringing their own careers. Banks are not fundamentally evil, they simply are the victims of a system design which rewards it.1.2 The limitations of lookback models when predicting the future

To ensure that assets match liabilities on a day-to-day basis, banks rely on control systems to measure past depositor behavior and establish margins within which the bank can continue to operate. Initially, this began as simply keeping a sufficient amount of cash-on-hand, or reserves, to buffer bank runs that might occur. As time has progressed, banks have evolved their balance sheet management to measure average inflows and outflows of deposits, laddering illiquid assets to match their projected capital outflows. The process of projecting these cash outflows began with simple averages, but as statistics and finance have evolved, has become an advanced process. In the present-day, banks utilize algorithms to measure holistic depositor behavior over time, with the most advanced systems utilizing AI, data science, and Machine Learning models to augment the bank’s risk management operations. However, all of these models suffer from a common flaw: they largely rely on look-back models. Look-back models use historic knowledge to predict what future events will occur. The assumptions that go into these models are that if something has happened, it will likely happen again, and if something has not happened, then it is unlikely to happen. They look to the past to predict the future, but the black-swan events that often precipitate a bank failure are by their nature unpredictable, and fundamentally break the assumptions that go into models of this design. While it is possible for banks to measure what the market is likely to do, current banking models do not permit depositors to tell banks exactly what they will do. As such, banks relying on lookback models are forced to be reactive rather than proactive, limiting their ability to predict cash flows effectively and respond to changing events in real-time.1.3 The socialized cost of coordination failure and bank runs

As a consequence of the duration gap existing, and bank balance-sheet assets not being immediately redeemable 1:1 for cash, depositors cannot all immediately retrieve their money from a fractional reserve system. It is this duration gap that allows for bank runs to occur and that gives rise to the coordination problem of fractional reserve banking. In the current financial reserve system, even banks that are fundamentally solvent may fall victim to a bank run when depositors are uncertain about the health of their investments and lack the ability to communicate effectively between them. A potential liquidity crisis, or even the perception for the potential of a liquidity crisis, leaves depositors with a prisoner’s dilemma: while it may benefit everyone involved to keep their funds in the bank and avoid triggering an insolvency crisis, there is a strong first-mover incentive for depositors to recover their funds early to avoid being left without access. Nobody wants to be the person who holds tight and loses everything. At their core, all bank runs are caused by this coordination problem - if depositors could perfectly coordinate their withdrawals to avoid over-stressing the bank’s reserves, bank runs would not occur and no insolvency would result. However, as that is not the case, bank runs and their resulting insolvencies have become an accepted part of the banking system. The most famous example of this coordination failure is Black Tuesday, in which many Americans flocked to banks to demand their cash after hearing about banks going under from bad debt created by margin trading, a mass rush of withdrawal requests led to somewhere between a third and one half of US banks collapsing, thrusting the United States into the Great Depression. In an attempt to stem these widespread financial losses, governments have spent decades trying to address the coordination problem. Mostly, they have attempted to limit depositor losses in the event of a bank failure by socializing losses across their native currencies. In the United States, this has resulted in all American banks being placed under the regulatory umbrella of the Federal Deposit Insurance Corporation, an entity designed to both oversee banks and offer bank depositors insurance. The FDIC enacts policies meant to ensure banks hold sufficient reserves while also composing their balance-sheets of high-quality assets. In the event of a bank failure, the FDIC takes over the bank, sells its balance sheet assets at a reduced price to other banks through private deals, and compensates for any remaining losses by printing money. This solution is inherently market-inefficient and will ultimately prove to be unsustainable. Placing government-appointed individuals in charge of determining the secondary price of balance-sheet assets results in poorly priced deals, while socializing losses through inflation simply transfers the losses of bankers to the American public. Making depositors whole at the cost of taxpayers serves as a band-aid rather than a preventive cure, and dissolving banks entirely throws out the proverbial baby with the bathwater, reducing competition for larger banks and encouraging monopolistic stagnation.1.4 Summarizing banking’s duration gap problem

Fractional reserve systems, by their very nature, result in the creation of duration gaps that demand an organized approach to banking, a model to predict what depositor outflows will be, and a methodology to address the coordination problem of fractional reserve banking. The current banking system has addressed these problems as best it can with a top-down organizational approach, algorithmic look-back models, and a government-administered insurance framework. Yet these solutions are lacking, as they result in perverse incentives for bankers, in models that are purely reactive rather than proactive, and in government-sponsored insurance frameworks that serve only to socialize the cost of coordination failures rather than disperse them entirely. The existing banking system, with its centralized and hierarchical nature, is not good at measuring social consensus, nor at responding to it. Even innovations designed to side-step some of these issues, such as credit unions (better incentive alignment), still fall prey to the others. A new system is needed to address these three core issues with better solutions than have thus far been offered: InfiniFi offers that solution.2.0 Introducing InfiniFi

InfiniFi is a self-coordinated, depositor-driven fractional reserve system built to better address the challenges created by duration gaps in traditional banking, aligning incentives while securing greater returns without increased risk regardless of asset class. InfiniFi corrects the misalignment that has consistently destabilized banks by giving the platform’s key decision makers the most to gain or lose based on their decisions, while also offering depositors full transparency into the health and risk profiles of their investments. InfiniFi is also able to better measure market sentiment in real time by incentivizing depositors to become illiquid along a continuum of unbonding periods, creating a self-laddering system from which duration-matching can then be executed. This incentivization is driven by the distribution of returns from all balance sheet assets towards illiquid depositors, according to a multiplier assigned to them relative to their unbonding period. InfiniFi uses this market-sourced information to extrapolate current depositor preferences across liquid depositors as well, applying the self-similarity principle to discern their time preferences. Co-deployment of illiquid and liquid deposits into illiquid assets, according to fractional reserve principles, is utilized to increase rates of return for both liquid and illiquid participants above those available in respective traditional liquid and illiquid vehicles. To better handle coordination breakdowns, we introduce two features: an automated insurance backstop that grows more effective with every depeg and a liquidity pool to facilitate depositors directly exiting their positions, eliminating the need to sell balance sheet assets directly. We further delegate first-loss to the most illiquid depositors, those who have the most control over investment decisions in our system, which further aligns their incentives. Blockchain is chosen as the medium for InfiniFi because of its censorship resistance, its ability to improve social coordination through transparency, and the efficiency with which liquidity can be sourced through DeFi-based infrastructure.2.1 How InfiniFi Works: A technical case study

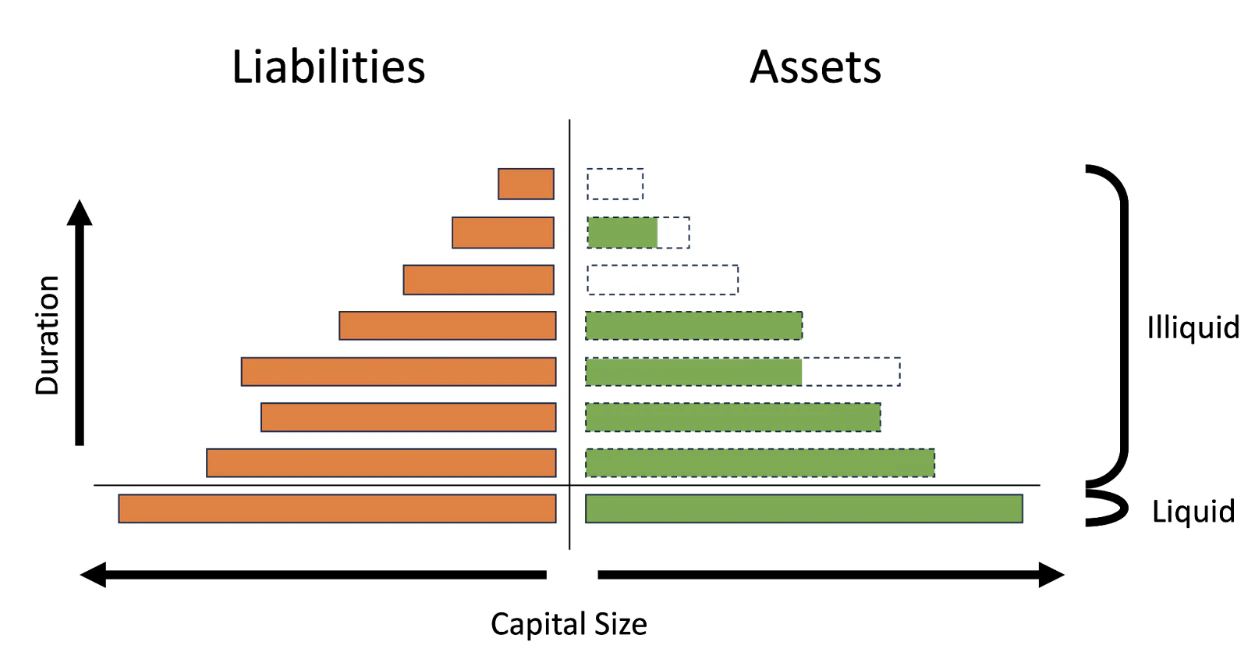

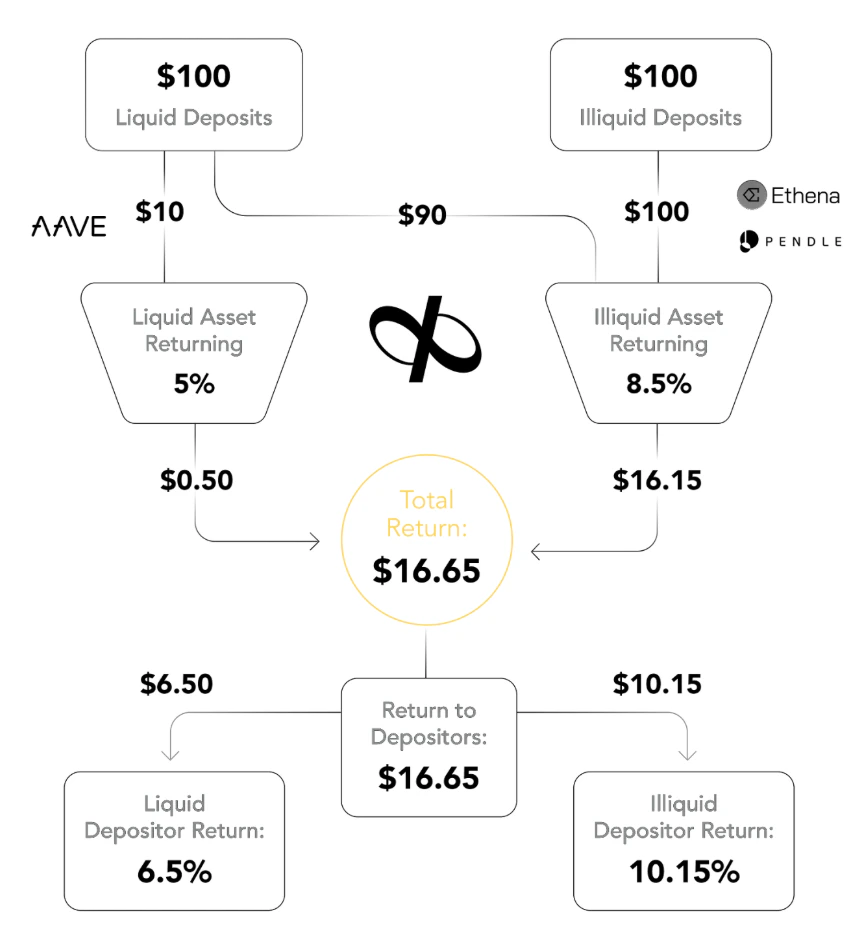

Any cryptocurrency asset can be deployed into InfiniFi. In this example, we will consider a dollar-pegged stablecoin like USDC. When someone deposits USDC into InfiniFi, they mint iUSD, and that deposit asset is immediately deployed to a trusted set of liquid vehicles. To achieve higher returns than depositing their assets on another platform — for example, a 5% return for depositing USDC to Aave — they must then bond their iUSD, with depositors self-selecting an unbonding period based on their time preferences (note: this is not how long their asset will be locked up for, but rather, how long it will be locked-up once they decide to begin unbonding). Depositors receive an ERC20 token to represent their bonded iUSD. To incentivize staking iUSD, InfiniFi awards depositors who stake for a longer period of time with a higher weighted-average time-multiplier. This is based on our weighting function — for example, if you agreed to a one-year unbonding period, you might receive a time-multiplier of two. We utilize that time-multiplier to calculate your weighted product. With that number calculated, we sum all weighted products together, and our weighted-average engine redistributes returns across depositors according to their fractional proportionality of the weighted product sum. For example, if you had 100 pool earning 10/5=10 as 110 pool, meaning you get 110*0.91 of interest. At this point, depositors who have chosen to become illiquid depositors are making more than liquid depositors (9.1% in this example); this might be an acceptable return, except now liquid depositors are making lower rates than they could receive from simply depositing into AAVE (4.45% here). To address this, we take advantage of the fact that many illiquid depositors have just shared their liquidity preferences with us by bonding their iUSD. Armed with this knowledge, the system is able to self-ladder. This process is depicted in Figure 1, where known illiquid liabilities of varying durations inform the acquisition of illiquid assets. Knowing how much capital is willing to bond for a given duration allows depositors to direct the acquisition of illiquid assets (for example, Pendle) that duration-match known illiquid deposits. USDC is withdrawn from AAVE and redeployed into these illiquid assets. To implement a fractional reserve system, improve returns for all participants, and increase capital efficiency, a proportion of the capital deployed to these illiquid assets is sourced from liquid depositors. What proportion of the capital deployed may be sourced from liquid sources is determined both by depositors themselves and by limitations imposed by the need to keep a certain amount of liquid capital on-hand at all times to satisfy a reserve-rate.

2.2 Deploying depositor assets

To address the need for laddering balance-sheet assets created by the duration gap, InfiniFi places depositors fully in charge of asset selection and allocation. By utilizing a bottom-up organization method over the more traditional top-down approach, InfiniFi corrects the incentive misalignment of traditional financial reserve banking by handing depositors complete transparency and control over the risk profiles of their investments. Illiquid depositors are given voting privileges proportional to the weighted product of their time-multiplier and their deposit size. These votes are then utilized to determine how much depositor capital is deployed to any given asset, liquid or illiquid. Amongst liquid assets, these votes determine what weighting any given liquid vehicle may have. With illiquid assets, these allocation votes determine how much capital will be allocated to a given illiquid asset (evergreen assets), or if any capital at all will be allocated in the case of assets that require a threshold to trigger the investment. Those locking the largest amounts of money for the longest periods of time have the most voting power in InfiniFi but also stand to lose the most from bad investment decisions, fully aligning their incentives to strike a balance between taking on risk and seeking higher returns.2.3 Matching assets to liabilities

InfiniFi also offers a better way to match assets with liabilities than the lookback models deployed by the traditional financial reserve system. InfiniFi incentivizes depositors to become illiquid by offering them greater returns, even attracting illiquid depositors on other projects to migrate their assets into InfiniFi and earn more as well (for instance, Pendle could be used as an illiquid asset, with the Pendle token holder serving as a new illiquid depositor, routing his existing deposit to Pendle through InfiniFi without changing his risk profile). This improves InfiniFi’s ability to close the duration gap by increasing the average duration of InfiniFi’s liabilities. Having more illiquid deposits means that InfiniFi can have higher reserve rates than traditional banks, improving stability, without sacrificing capital efficiency. In addition, InfiniFi’s self-laddering system allows for direct measurement of market sentiment. Rather than having to rely solely on predictive control systems to guess at cash inflow and outflow rates, InfiniFi incentivizes depositors to tell InfiniFi their direct future intentions. While predictive control systems will likely bring even higher capital efficiency and functionality to InfiniFi, the fact remains that direct knowledge of the future is always more efficient than guesswork. InfiniFi is further able to achieve stability through the self-similarity principle. In alignment with this principle, InfiniFi operates under the assumption that the holistic liquidity preferences of both the illiquid and liquid depositors will be roughly equivalent (in most cases, whether a depositor is liquid or illiquid will have more to do with how active they want to be on InfiniFi rather than a difference in liquidity preferences). Based on this assumption, InfiniFi can get better insights into the capital availability needs of its liquid depositors, using the information it has already gathered from its illiquid ones. This knowledge further reduces the likelihood of a depeg event, in which depositors are temporarily unable to redeem iUSD (such events, while rare, are to be expected, and InfiniFi has a number of ways to address them).2.3 Managing Bank Runs and Bad Debt

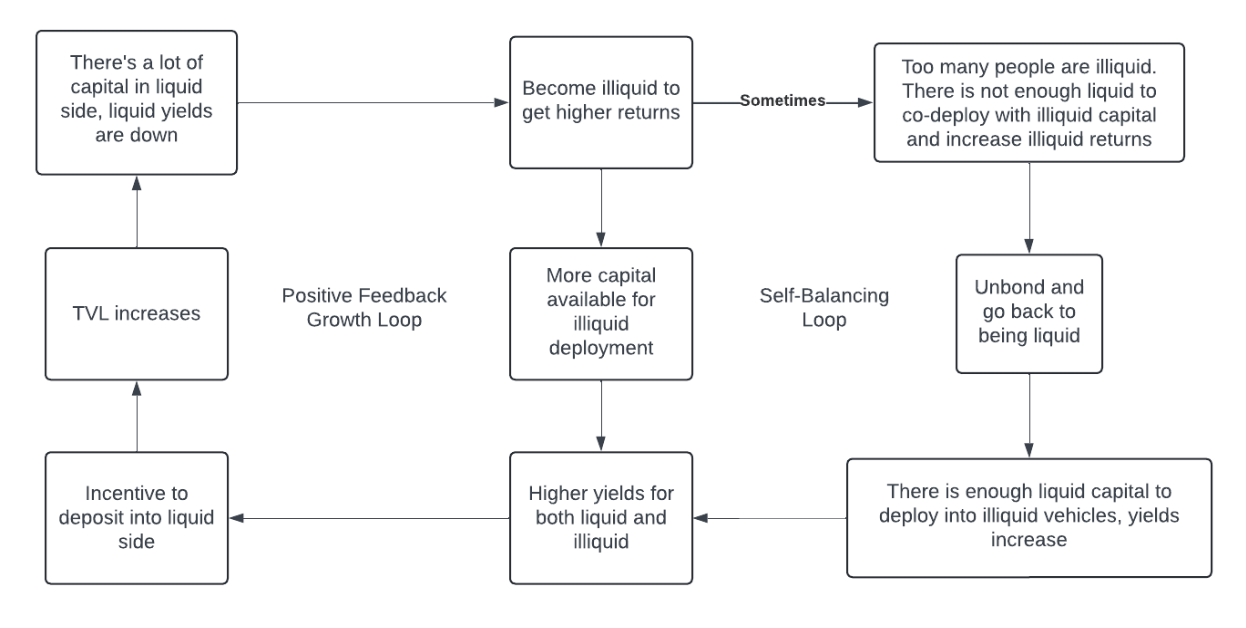

In finance, as in all business, things eventually go wrong. It is how systems respond that dictates their resilience. When coordination failures do occur, when illiquid assets default, InfiniFi must not be placed in a permanent failure mode. To address the question of what to do when things go wrong, InfiniFi establishes first-loss principles and automates the process of finding buyers-of-last resort through a Curve stableswap pool. In the unlikely event that an illiquid vehicle that InfiniFi depositors have directed capital into defaults, InfiniFi may first attempt the sale of the bad debt on the secondary market to recover some capital. Whether capital is recovered or not, the remaining losses are then socialized to InfiniFi illiquid depositors proportional to their voting power —- those with the highest voting power are socialized a larger proportion of the loss than those with lower voting power. As long as illiquid deposits exist to absorb losses, liquid depositors remain fully insulated from losses. This model strongly aligns incentives for those with the most voting power to refrain from excessive risk taking — while they receive the highest returns as a result of their high voting power, they also receive the highest losses in the event of default. Through additional safeguards, such as caps on concentration of capital across a single protocol or investment vehicle, InfiniFi offers a mechanism design that incentivizes depositors to acquire a lower-risk and diversified basket of assets on InfiniFi’s balance sheet, over ones that risk permanent insolvency. Still, for all of InfiniFi’s advances in direct measurement of market will, increased illiquidity of depositors, and duration matching of public sentiment, coordination failures can occur. In the event that liquid depositors begin to cash in, this leads to a reduction of capital in the liquid pool, resulting in yields for liquid depositors increasing. Under typical circumstances, this is itself enough to encourage additional depositors to deposit their capital into InfiniFi and replace those leaving (particularly if lending markets and leverage loops exist). However, during certain events, this will be insufficient, and all liquid reserves in InfiniFi will be exhausted. To tackle this eventuality, InfiniFi will incentivize liquidity onto Curve stableswap pools, using deliberately segregated streams of its emissions to attract LPs (eventually acquiring its own protocol-owned liquidity). A further discussion of this incentivization may be found in the Governance section. The existence of an automated secondary market for iUSD liquidity will facilitate automated provisioning of buyers-of-last resort for depositors during a temporary insolvency. Rather than the closed-door methodology employed by conventional deposit insurance frameworks — which operate by seizing and selling illiquid assets held on a balance sheet at an artificially determined price — InfiniFi uses AMM technology to facilitate a fair-market price for InfiniFi’s liquid liabilities. Multiple case-studies in DeFi have shown that when fully-backed assets become temporarily insolvent, the result is never total collapse, but rather, temporary trading below peg. One classic example of this is USDC, which was temporarily insolvent over a weekend in March of 2023. The well-reputed stablecoin depegged to $0.74 amidst concerns over insolvency, giving many arbitrageurs the opportunity of a lifetime to purchase a dollar at less than a dollar. Once redemptions resumed Monday morning, the token quickly re-pegged, and all who bought below peg made significant profit. Another well-known example, for a far-longer period, of temporary insolvency, is Lido’s well-known liquid staking token, Staked Ether (stETH). While stETH was known to have a 1:1 backing for much of its existence, it was not possible to redeem this backing until after the Ethereum Merge in early 2023. Prior to this, stETH frequently traded below its 1 ETH peg, trading in 2022 at as low as 0.9 ETH. Despite this, people continued to use stETH, and when the Merge occurred, those who had purchased below-peg reaped the benefits. When protocols that are fully backed become temporarily insolvent, the result is not collapse, but opportunity, and that is precisely the mechanic that InfiniFi takes advantage of during depeg events. Not wanting to let all profit from depegs go solely into the hands of arbitrageurs, InfiniFi implements an active mechanism designed to guard the peg, growing larger with every depeg.2.4 Summarizing InfiniFi’s innovations

InfiniFi offers a novel approach to solving the problems of the financial reserve system. Its depositor-driven system better aligns incentives, closes the duration gap beyond what traditional banking is capable of through direct market knowledge, and facilitates the efficient handling of both bad debt and temporary insolvency events through DeFi-native architecture. All this is accomplished while providing depositors with higher returns than they would be able to access for any given liquid or illiquid yield source, passing along the improvements in capital efficiency that would typically be absorbed as profit in the traditional banking world would be absorbed entirely as profit. InfiniFi offers a vision for the future of banking in which risks are properly weighed with returns, in which depositors can begin to conceive of fractional reserve practices as a beneficial practice rather than an odious insider’s game, and in which banking benefits primarily those who trust it with their hard-earned money. To realize this vision, InfiniFi introduces a series of mechanisms that have their own second and third order implications. To manage these implications, and preserve the benefits of InfiniFi for years to come, InfiniFi introduces further systems to provide for its decentralized, on-chain governance.Governance

To fully address governance is a whitepaper unto itself. This whitepaper is currently being written, and prior to it being merged into this paper, the outline describing governance functionality shall suffice.Why is Governance Needed?

How will capital be deployed? Who decides where capital can be deployed? Tragedy of the Commons problem Hijacking of funds must be avoided How to incentivize early adopters? How to incentivize liquidity providers?Non-Governing Roles

Protocols - propose a new parent adapter for different product offerings May take a cut of proceeds from adapter Subject to audit requirements May be subject to bond requirements Must pay a fee in utility token to submit Proposers - propose new product offerings from a parent adapter May take a cut of proceeds from product Keep offerings on InfiniFi up-to-date with protocol offerings MEV expected to dominate Put up bond if required for parent adapter Must pay a fee in utility token to submitAllocators

Allocators direct funds to illiquid vehicles, reserves deployed according to a set proportion Also vote on liquid vehicle composition Capital delegated according to voting power Depositors being in-charge produces better incentive alignment Voting system of individuals and delegates One-layer deep Agents will eventually be automated (AI) Delegated votes must arrive one day before individual ones and can be erased during a 24 hour grace period, during which individuals can un-delegate if they do not like outcome To receive their emissions, Allocators must: If solo voters, vote weekly If delegated voters, their delegates must vote on their behalf. Delegates get a cut of emissions from their delegators.Verifiers

Introduce token Concept of Verifiers Approve protocols Approve specific products created from Protocol adapters by Proposers May include max size (non-evergreen) May include maturity (illiquid fixed-maturity) May include duration (illiquid fixed-duration) Economic difficulty of acquiring 51% of the tokens Voting rights gained by Staking tokens with one-week unbonding period Burning tokens to permanently bind them to an illiquid position (more later) Voting incentivized by desire to not lose value in token or money in deposits Voting system of individuals and delegates One-layer deep Delegated votes must arrive seven days before individual ones and can be erased during a seven day grace period, during which individuals can un-delegate if they do not like outcome Delegates receive additional bonus to Loyalty Multiplier on a single position, dependent on how much power has been delegated to them Diminishing returns to discourage centralization Increase to bias (up/down)Token Gamification and Emissions

Emissions on a long-tail decay curve Loyalty Multiplier concept Linearly increases while you are bonding Increase to voting power, earnings, and emissions Can be permanently increased in step-function by burning utility token Game theory - Financialization of “being early” Sell Burn Stake Hold Bias can be additionally increased/decreased by delegated Verifier powerVetoers and Election System

Vetoers can kill any adapter or product proposal Only one out of five (⅕) needed to kill a proposed offering Can ban addresses from being Proposers or Protocols, contracts from being adapters, bytecodes from being accepted One member up for reelection every year Challenger must reach 75% of the vote to win, otherwise incumbent remains If multiple parties in election, worst 75% eliminated, vote re-held ⅘ Vetoers may remove a single Vetoer and trigger an election Special period, new adapters not accepted until 5/5 present Voted on by Verifiers and Allocators with each side equally weighted Makes attacking Vetoer system to steal deposits extremely difficultTreasury, Design Parameters, and Incentive Management

Treasury Pool financed by small fee on interest Management of both reserved for Allocators Deployment of Treasury managed by Allocators Incentive Management Allocators incentivized to use Treasury for POL acquisition Certain amount of emissions set-aside for: Liquidity on stablecoin Liquidity on utility token Design Parameters Require a high margin to pass changes (66%+)3.0 Virtuous cycles for modern finance

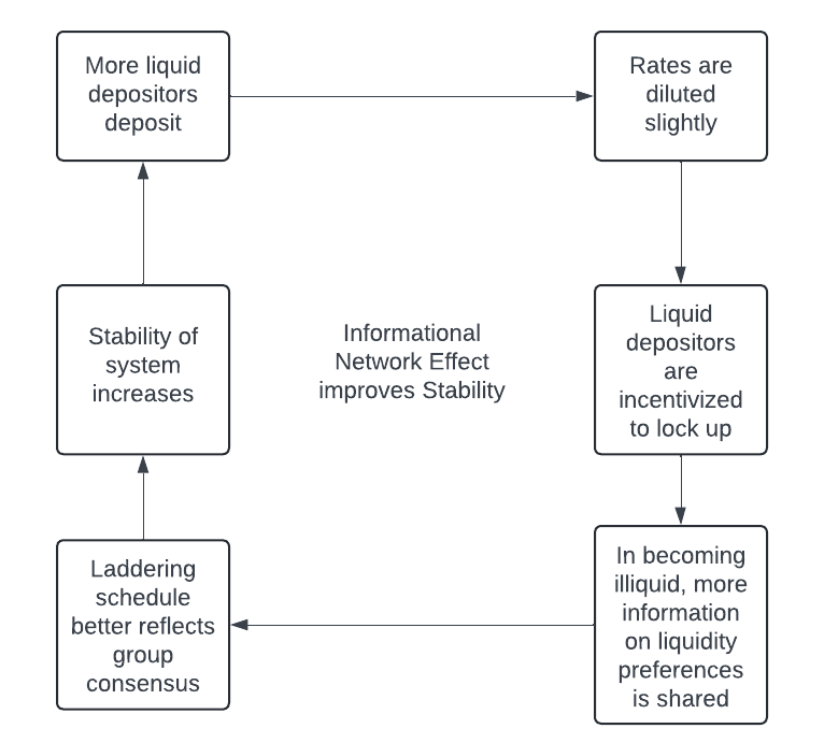

InfiniFi’s novel structure creates a series of flywheel effects for depositors and the network that helps them earn more for investing their hard-earned assets on it as more participants join in. For a financial enterprise, flywheel-effects, where positive-feedback cycles play-off their own success, are critical to long-term success and growth. InfiniFi possesses two such flywheels: one dealing with the positive-feedback loop between rates and TVL and the other describing InfiniFi’s network effect.3.1 The positive rate-TVL feedback loop

3.2 The information network effect